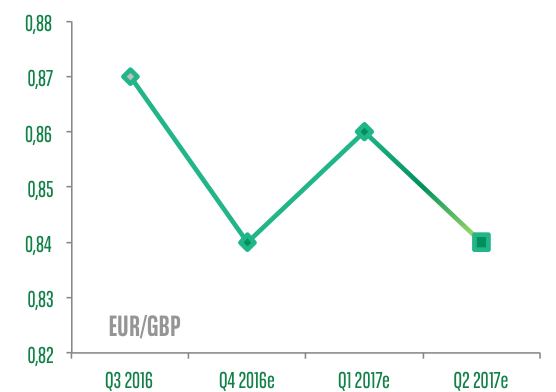

Only a few months after the UK referendum, one

might be tempted to label the Brexit vote an economic non-event. However it is

far too early to measure the consequences – other than its

downward pressure on sterling. The UK’s challenge lies in continuing to attract

international investors, at a time when the country risks losing access to the

European market.

The task will be particularly tough, given that public

finances are expected to deteriorate and monetary policy is aimed at keeping

interest rates low.

These factors ultimately signal a long depreciation of the

pound.

")

The upturn in energy prices is likely to continue to increase inflation in the coming months via base effects. We expect headline inflation to exceed 1% as of Q1 2017.

Abenomics has been bolstered again, with the government announcing renewed spending efforts. The Bank of Japan also made a firmer commitment to improving inflation via new measures.

") |

|

Expectations of a difficult and costly Brexit have considerably undermined the British Pound. Since the referendum, the nominal effective exchange rate of sterling has fallen 12%. This pressure on GBP is bound to persist.